This post is motivated by recent headlines suggesting that the Chinese yuan has depreciated in recent days. Here’s an example: China’s yuan weakens to 5-1/2 low as c.bank tolerates depreciation. This headline is completely inaccurate – the Chinese yuan has been appreciating in recent days. So that’s one problem I’d like to fix.

Read More »2016-07-05

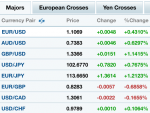

(1.3.) Let’s improve the way we report FX rates