Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?15 Apr 2024

Weekly Market Pulse: Monetary Policy Is Hard

Weekly Market Pulse: Monetary Policy Is Hard6 Nov 2023

Macro: Sep CPI stuck at 3.7% YOY

Macro: Sep CPI stuck at 3.7% YOY13 Oct 2023

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!13 Feb 2023

Weekly Market Pulse: Happy Days Are Here Again!

Weekly Market Pulse: Happy Days Are Here Again!7 Feb 2023

Weekly Market Pulse: First, Kill All The Speculators

Weekly Market Pulse: First, Kill All The Speculators31 Jan 2023

Weekly Market Pulse: A Fatal Conceit

Weekly Market Pulse: A Fatal Conceit24 Jan 2023

Here are three things you can learn from the Fed

Here are three things you can learn from the Fed13 Jan 2023

How To Design Corporate Budget For A Growing Company

How To Design Corporate Budget For A Growing Company9 Jan 2023

Weekly Market Pulse: The Consensus Will Be Wrong

Weekly Market Pulse: The Consensus Will Be Wrong9 Jan 2023

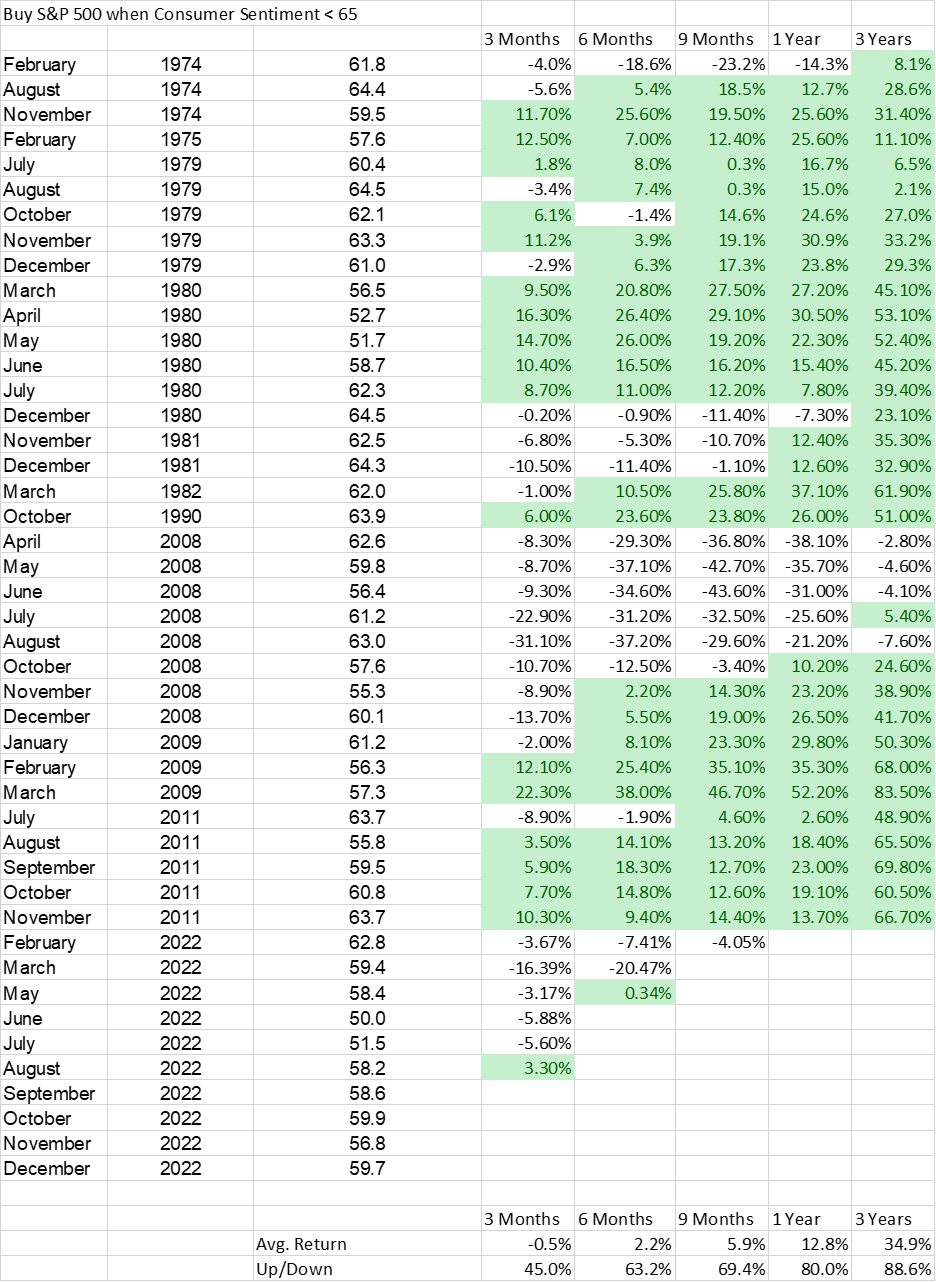

Great News! Consumer Sentiment Is Awful!

Great News! Consumer Sentiment Is Awful!4 Jan 2023

Weekly Market Pulse: Happy Holidays

Weekly Market Pulse: Happy Holidays20 Dec 2022

Weekly Market Pulse: Envy

Weekly Market Pulse: Envy12 Dec 2022

Ep 50 – Brent Johnson: Has the Dollar Milkshake Spilled or Just Begun?

Ep 50 – Brent Johnson: Has the Dollar Milkshake Spilled or Just Begun?6 Dec 2022

Weekly Market Pulse: Currency Illusion

Weekly Market Pulse: Currency Illusion28 Nov 2022

Weekly Market Pulse: Good News, Bad News

Weekly Market Pulse: Good News, Bad News14 Nov 2022

The Cleanest Dirty Shirt

The Cleanest Dirty Shirt28 Oct 2022

25 Oct 2022

Weekly Market Pulse: Did Powell Just Blink?

Weekly Market Pulse: Did Powell Just Blink?24 Oct 2022

Market Currents: Fed Confusion

Market Currents: Fed Confusion20 Oct 2022

Is Gold Starting to Behave Itself?

2022-05-14

by Stephen Flood

2022-05-14

Read More »