Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

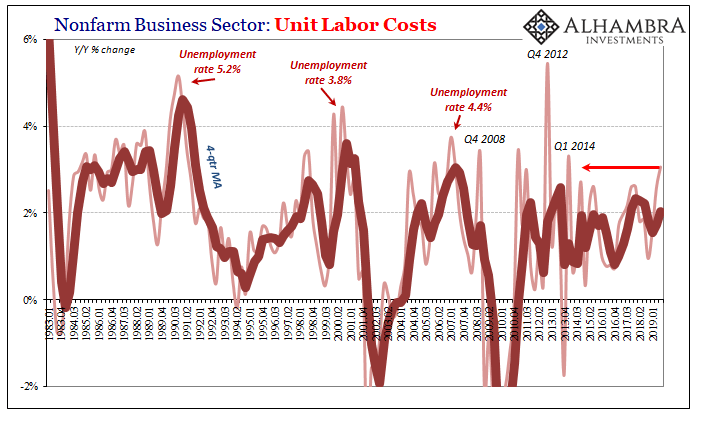

Immigration And Its Impact On Employment

Immigration And Its Impact On Employment12 Apr 2024

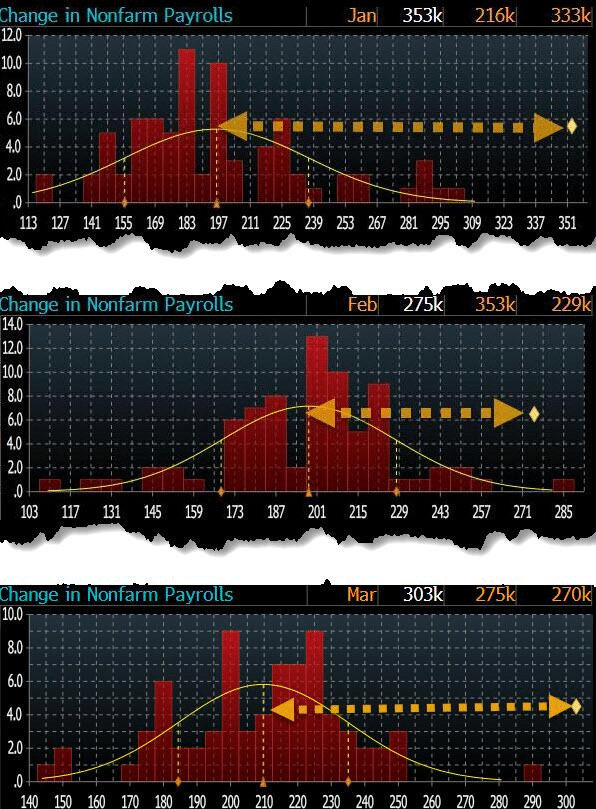

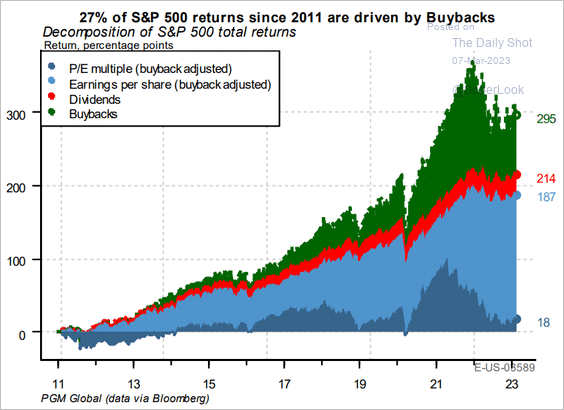

Blackout Of Buybacks Threatens Bullish Run

Blackout Of Buybacks Threatens Bullish Run19 Mar 2024

Digital Currency And Gold As Speculative Warnings

Digital Currency And Gold As Speculative Warnings12 Mar 2024

Presidential Elections And Market Corrections

Presidential Elections And Market Corrections10 Mar 2024

Valuation Metrics And Volatility Suggest Investor Caution

Valuation Metrics And Volatility Suggest Investor Caution5 Mar 2024

Fed Chair Powell Just Said The Quiet Part Out Loud

Fed Chair Powell Just Said The Quiet Part Out Loud16 Feb 2024

Market Morsels: ISM and Recession

Market Morsels: ISM and Recession7 Feb 2024

Rethinking “safe” investments

Rethinking “safe” investments2 Nov 2023

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!13 Feb 2023

Weekly Market Pulse: Happy Days Are Here Again!

Weekly Market Pulse: Happy Days Are Here Again!7 Feb 2023

CEO Keith Weiner Quoted in Barron’s

CEO Keith Weiner Quoted in Barron’s3 Feb 2023

Weekly Market Pulse: First, Kill All The Speculators

Weekly Market Pulse: First, Kill All The Speculators31 Jan 2023

Poor US Data Cast Doubts on New Found Hopes of a Soft-Landing

Poor US Data Cast Doubts on New Found Hopes of a Soft-Landing19 Jan 2023

Weekly Market Pulse: The Consensus Will Be Wrong

Weekly Market Pulse: The Consensus Will Be Wrong9 Jan 2023

Weekly Market Pulse: Good News, Bad News

Weekly Market Pulse: Good News, Bad News14 Nov 2022

Weekly Market Pulse: Same As It Ever Was

Weekly Market Pulse: Same As It Ever Was22 Aug 2022

Will Silver Prices Go Up to $300?

Will Silver Prices Go Up to $300?11 Aug 2022

Weekly Market Pulse: Opposite George

Weekly Market Pulse: Opposite George1 Aug 2022

Inflation Crisis 2022 – Marc Faber Interview (Full)

Inflation Crisis 2022 – Marc Faber Interview (Full)21 Jul 2022

Euro Parity Holds ahead of US CPI

Euro Parity Holds ahead of US CPI13 Jul 2022