Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

8 Apr 2024

1 Mar 2024

Dollar Jumps

Dollar Jumps28 Feb 2024

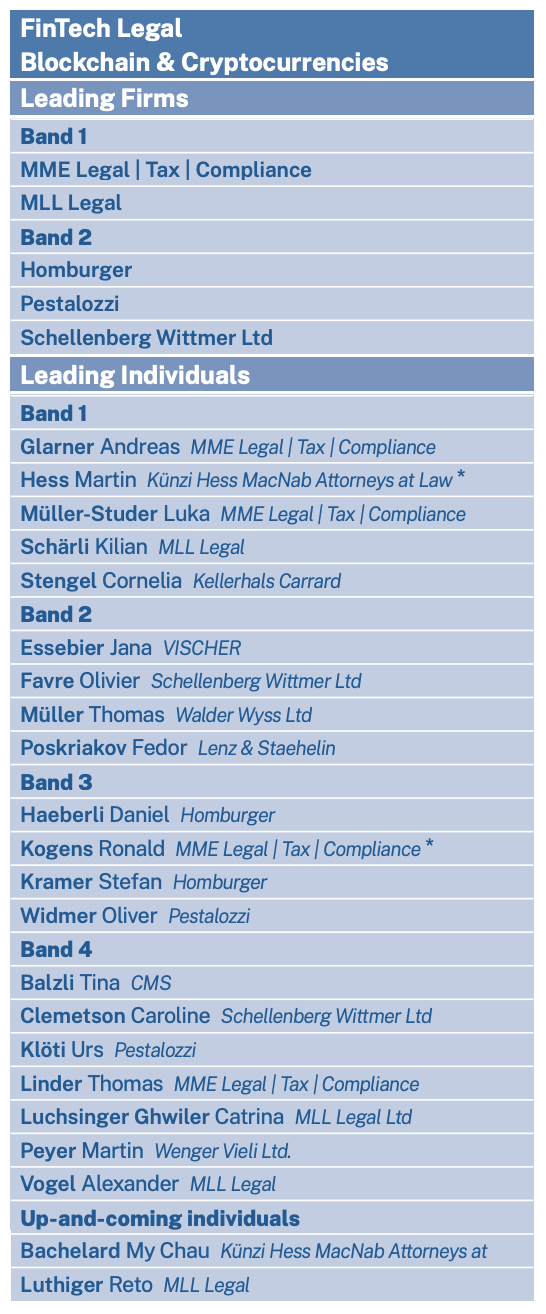

The Top Swiss Law Firms for Fintech and Blockchain Practice

The Top Swiss Law Firms for Fintech and Blockchain Practice22 Feb 2024

Quiet End to a Busy Week

Quiet End to a Busy Week16 Feb 2024

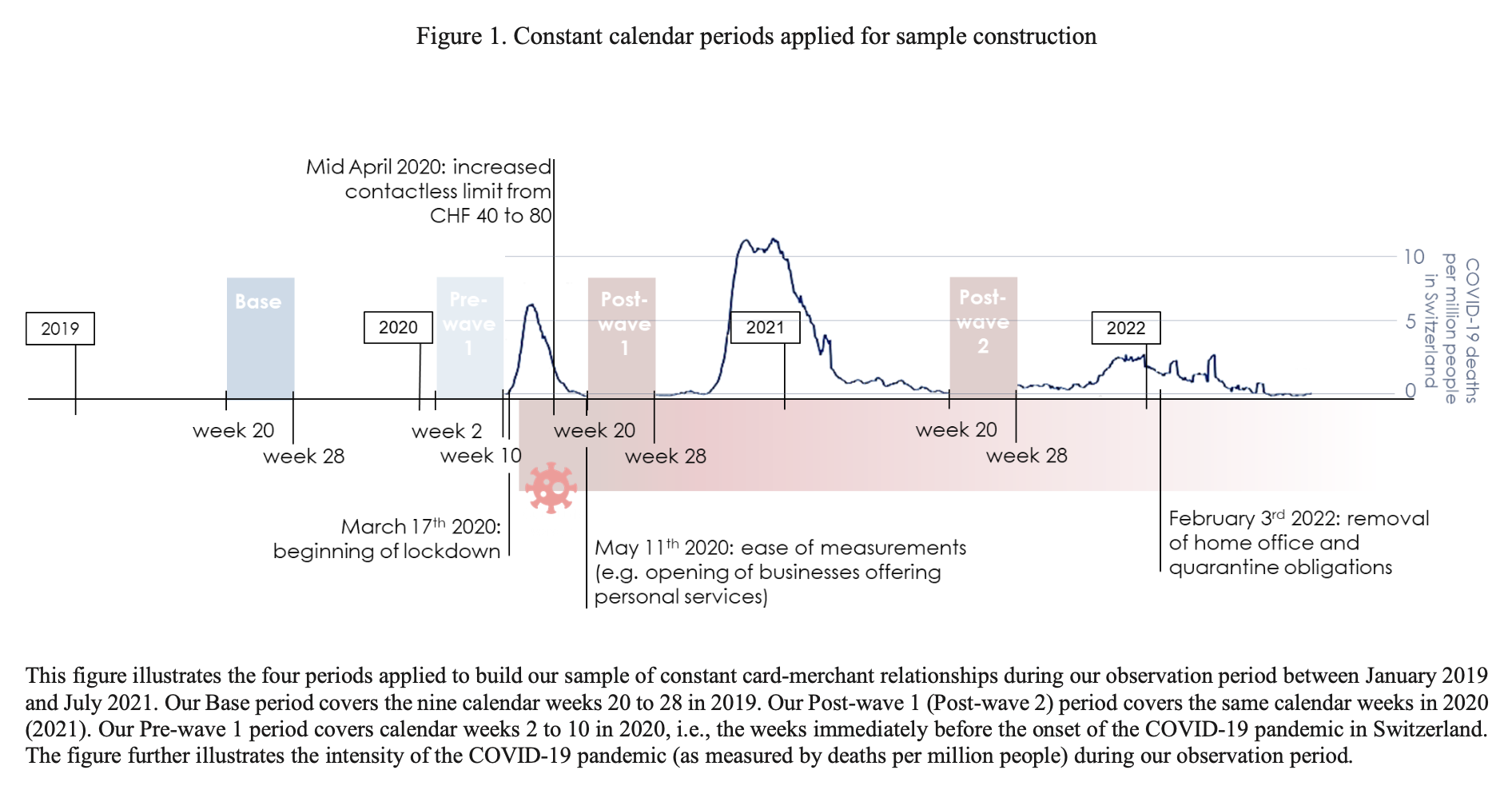

New SNB Study Reveals Critical Role of Card Schemes and Banks in the Contactless Payment Usage

New SNB Study Reveals Critical Role of Card Schemes and Banks in the Contactless Payment Usage12 Jan 2024

Holiday Moves Continue to be Unwound

Holiday Moves Continue to be Unwound3 Jan 2024

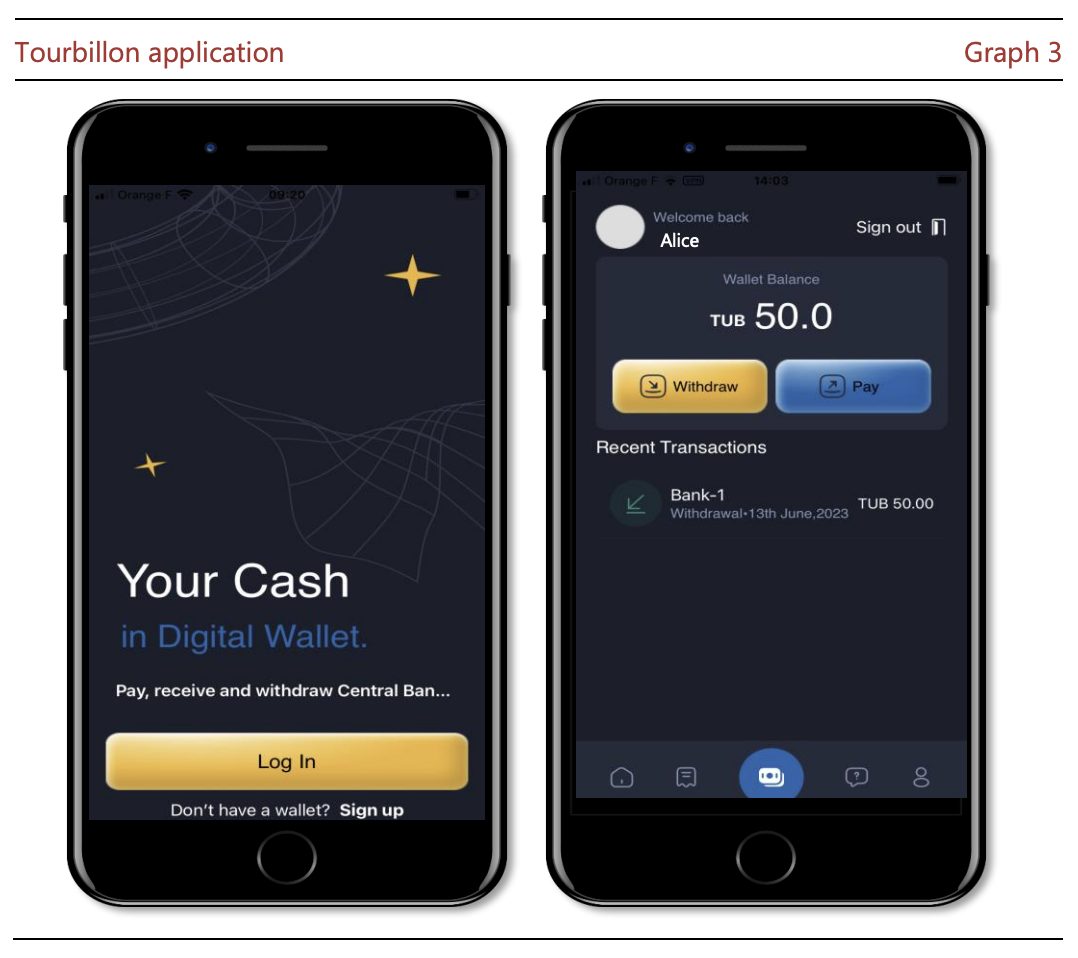

Swiss-Backed CBDC Project Explored Feasibility of Cash-Like, Anonymous Digital Currency

Swiss-Backed CBDC Project Explored Feasibility of Cash-Like, Anonymous Digital Currency21 Dec 2023

Markets Catch Collective Breath

Markets Catch Collective Breath6 Dec 2023

22 Nov 2023

16 Nov 2023

Food Prices Drive China’s CPI Lower while the Greenback is Mostly Firmer in Narrow Ranges

Food Prices Drive China’s CPI Lower while the Greenback is Mostly Firmer in Narrow Ranges9 Nov 2023

Swiss Banks Unlikely to Migrate to Blockchain, DLT Systems, Says SNB Advisor

Swiss Banks Unlikely to Migrate to Blockchain, DLT Systems, Says SNB Advisor2 Jun 2023

Consolidative Session Marked by Weak Chinese Imports and White House Debt Ceiling Talks

Consolidative Session Marked by Weak Chinese Imports and White House Debt Ceiling Talks9 May 2023

Bank Stress Hobbles the Dollar, while Dissents Make the 50 bp Hike by Sweden less than Hawkish

Bank Stress Hobbles the Dollar, while Dissents Make the 50 bp Hike by Sweden less than Hawkish26 Apr 2023

Swiss Central Bank Payment Vision Outlining Focus on DLT, Tokenization and Instant Payments

Swiss Central Bank Payment Vision Outlining Focus on DLT, Tokenization and Instant Payments13 Apr 2023

10 Apr 2023

Firmer Rates and Higher Bank Stocks Give the Greenback Little Help

Firmer Rates and Higher Bank Stocks Give the Greenback Little Help28 Mar 2023

Yields Pull Back to Start the New Week

Yields Pull Back to Start the New Week6 Mar 2023

Markets Catch Collective Breath

Markets Catch Collective Breath16 Feb 2023